Q4 2020 Truckload Market Forecast: Coyote Curve Guide to Volatility

With the most volatile year in our recorded history coming to a close, we’re able to get a clearer picture of how COVID-19 has shaped the U.S. truckload market in 2020.

In this update of the Coyote Curve®, we’ll take a look at activity through the first three quarters and discuss a path forward into 2021.

- Q3 Truckload Market: Spot & Contract Rate Trends

- Where We Are in the Capacity Cycle

- Q4 Forecast

- Recommendations to Thrive in Peak

- Q4 Coyote Curve Webinar

New to the Coyote Curve?

The Coyote Curve is our proprietary spot rate index built with data from over 10,000 daily shipments. If you want to learn more about the truckload market or how we build the Curve, check out these helpful guides:

Part 1: Understanding the U.S. Truckload Market

Part 2: Explaining the Coyote Curve

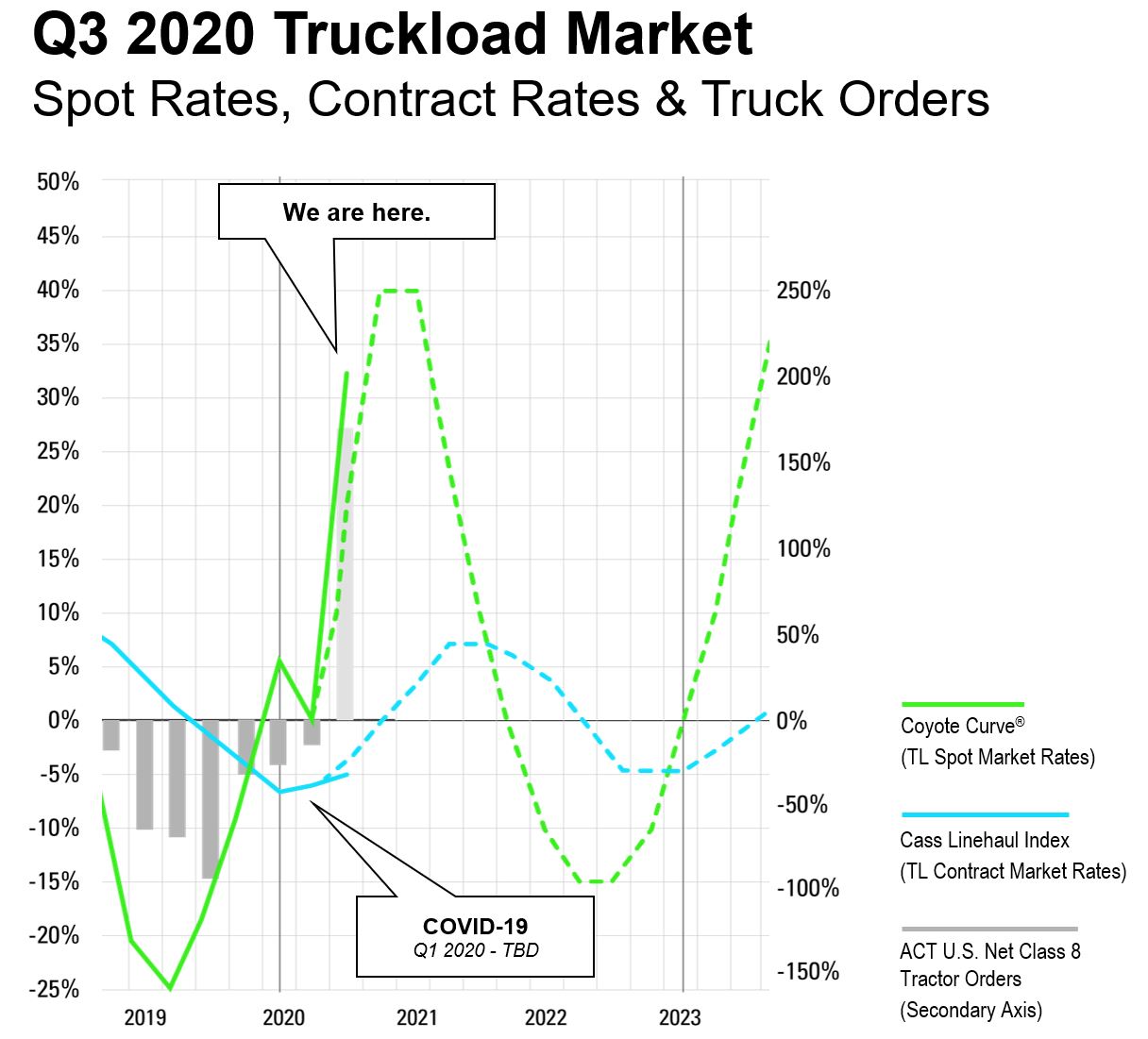

Q3 2020 Truckload Market Performance

Q2 2020 was the most volatile quarter in the history of the Coyote Curve index. Throughout the quarter, spot rates reach dizzying heights and deep lows. By the end of the quarter, the net result was, oddly enough, a return to equilibrium (0.0%).

In Q3, with many of the government shutdowns lifted, we saw a surge in shipping activity, bringing the Curve index back along the path towards an inflationary peak.

Instead of a fundamental shift in the truckload market capacity cycle, the COVID-19 pandemic created a kink in the line.

Q3 Truckload Spot Rates Are Trending Upwards

- Q3 2020 spot rate performance: 35.2% Y/Y

- Trending Up from Q2 (0.0% Y/Y)

- Q3 was directionally in-line with our Q2 forecast, but the rate of increase was even steeper than anticipated

Q3 Truckload Contract Rates Are Trending Upwards

- Q3 2020 contract rate performance: -5.1% Y/Y

- Trending up from Q2 (-6.0% Y/Y) but still trailing 2019 performance

- Q3 was directionally in-line with our Q2 forecast, trending up for the 2nd consecutive quarter after 7 quarters in decline

Current State of the U.S. Truckload Market: It’s Volatile (and Peak Season Won’t Help)

Demand (Shippers)

Rapidly changing consumption patterns are leading to unprecedented volatility on the demand side — some shippers are surging, some are slumping.

Considering raw material suppliers all the way through finished goods shippers, there are many areas for disruption across long, often international, supply chains.

Supply (Carriers)

The sharp economic recession had a significant impact, tightening capacity as many carriers shut down part — or all — of their fleets.

Since ~90% of the nation’s carrier base consists of small businesses without easy access to capital, it isn’t necessarily simple to bring capacity back on the road just because spot rates are shooting up — many smaller carriers are still hurting from a soft April and May.

Volatility is Driving an Increase in Spot Rates

Both demand volatility and capacity constraints are inflationary catalysts, driving up spot rates in the U.S. truckload market.

There have been pockets of supply/demand dislocation, causing a lot of operational pain. For example, we’ve seen load times increase as shippers struggle to effectively manage trailer pool equipment in drop yards.

Shipper demand is spiking (unevenly), carrier capacity is tight, spot rates are shooting up and volatility reigns supreme.

Increased Q3 Consumption Is Driving Activity

Through Q3, both the economy and the truckload spot market have reacted as if Q2 was a coiled spring. The federal and state government shutdowns deferred consumption and in Q3, we saw this potential energy released.

Inventories are dropping, hitting a five-year low as people start to reengage in the economy and shippers hesitate to drop capital in building inventory back up.

Sales and consumption are happening, they’re just happening in different ways; less brick and mortar, more e-commerce, less on-premise services, more at-home consumption.

“Most of the post-April economic data points are increasingly positive, and that makes me pretty optimistic.”

-Chris Pickett, Strategic Advisor, Coyote Logistics, in the Q4 Coyote Curve Market Forecast Webinar

“Most of the post-April economic data points are increasingly positive, and that makes me pretty optimistic.”

“Most of the post-April economic data points are increasingly positive, and that makes me pretty optimistic.”

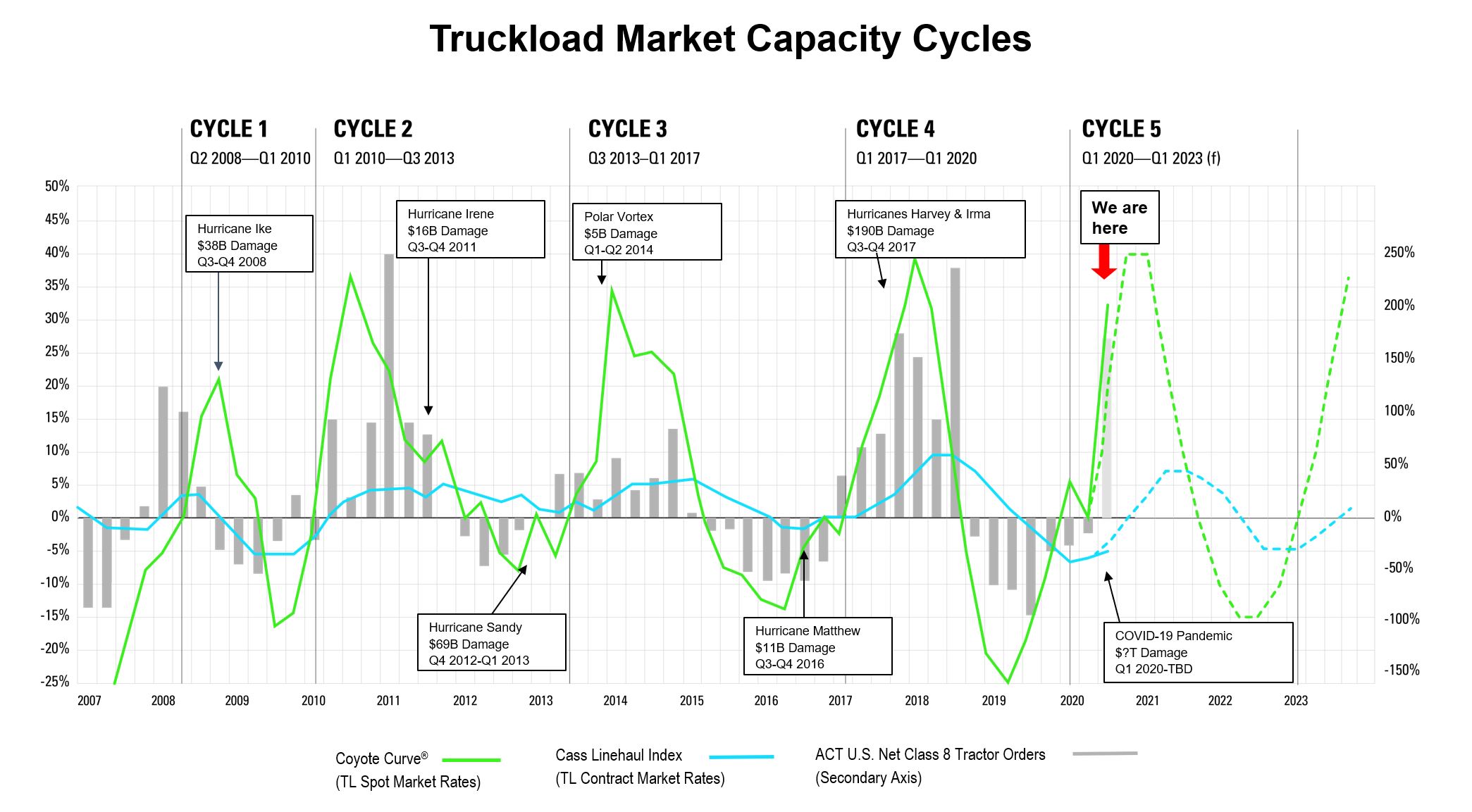

Where We Are in the Cycle: Inflationary & Heading Towards a Peak

Right now, we are in the inflationary leg of the market capacity cycle, heading towards a market peak.

In early 2020, as carriers stared into the abyss of a sharp economic recession due to COVID-19, they were understandably hesitant to make long-term capital expenditure decisions.

Long story short: carriers held off on investing in additional capacity for a couple quarters (looking specifically at the gray bars).

However, now that spot rates are climbing higher, and will likely continue to do so over the next quarter at least, we can see carriers adding capacity again, as Q3 truckload orders spiked.

This is likely setting the stage for the supply overshoot that will eventually lead to the next market trough.

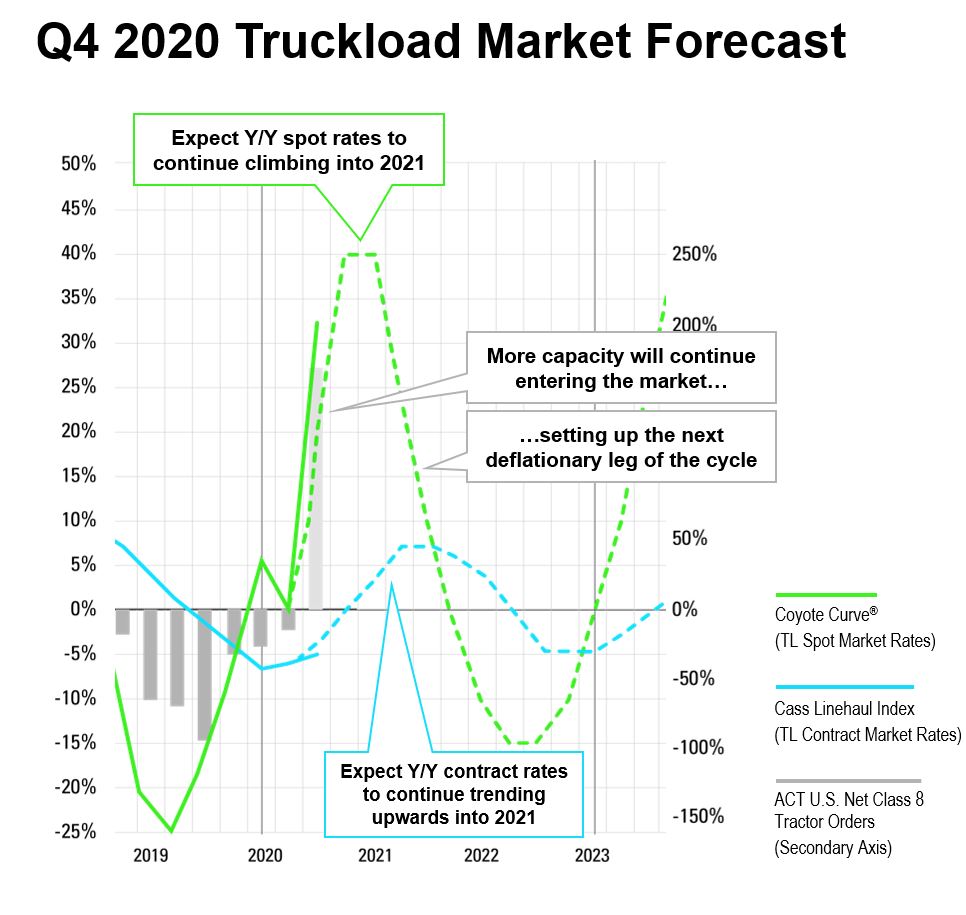

Q4 2020 Truckload Market Forecast

Peak season is upon us. With the pandemic-driven boom in e-commerce, it promises to be a high-volume one, creating even more volatility as demand increases while carrier supply scrambles to keep up.

Furthermore, rising COVID-19 infection rates will create more uncertainty across the economy. Combined with a pending vaccine (and subsequent distribution), it all adds up to — you guessed it — market volatility.

We expect year-over-year spot rates to continue climbing into 2021 before reaching another market peak. We also anticipate contract rates to continue climbing, getting back into year-over-year positive territory by Q1 of 2021.

Supply Chain Strategies to Thrive in Peak

You will not be able to completely insulate yourself from some volatility over the next few months, but incorporating the following strategies can mitigate your exposure:

Get as digitally connected to your transportation providers as possible.

Make sure your systems talk to each other — the more API the better. Consider upgrading your TMS software if it isn’t providing enough operational flexibility.

Over-communicate your forecasted shipping needs with your core providers.

This is true in any market, but especially important in the current environment. Even if you are less confident than usual, the more open and honest you can be, the better you will position your business in the coming months.

Flexibility is the name of the game.

Anywhere you can add flexibility to your network, do it. Consider providers with alternative capacity solutions.

Experiment with shorter bid cycles.

Try out quarterly instead of annual, monthly instead of quarterly on strategic portions of your network. The more accommodating you can be as a shipper, the better service you’re going to get.

Double-down on trusted providers in your 2021 RFP.

Bid season is right around the corner. As you prepare for your RFP, evaluate your current contract rate versus spot rate exposure, then compare that against the rate environment we expect for next year. Where possible, lean on your core providers to protect you against unplanned exposure to the spot market.

This Too Shall Pass

If we have learned anything over several years of tracking the Coyote Curve, it’s that history may not always repeat, but it certainly rhymes — the truckload market cycle will continue to move as it always has.

Remember that it’s in the peaks and the valleys where most of the bad decisions get made. Don’t panic, this too shall pass. Maintain a commitment to a long-term shipper of choice strategy, lean on your core providers and prioritize flexibility.

This market guide took insights from our recent webinar at the Coyote Logistics Digital Summit. You can watch the full Q4 Coyote Curve webinar on demand, which featured Coyote leaders as well as Evan Armstrong, President & CEO of Armstrong & Associates, the premier 3PL research firm.